This is the second consecutive year that Global Custodian and Intertrust Group have joined forces to undertake a survey exploring the changes private capital CFOs anticipate in their role in the years ahead.

Please click here to download the report – The future private capital CFO: Unleashing potential in the ESG era.

Building on many of the themes of last year’s exercise, the latest survey included an optional section on ESG, which shone a light on the growing importance of ESG in the investment process, probing both levels of engagement with ESG and challenges to implementation.

The survey recorded 320 validated responses from CFOs or their direct reports across USA, UK, China and Western Europe. In a parallel survey against which to test CFO assumptions, 110 investors in private capital funds – mainly in US, UK and China – were canvassed for their views on the same themes.

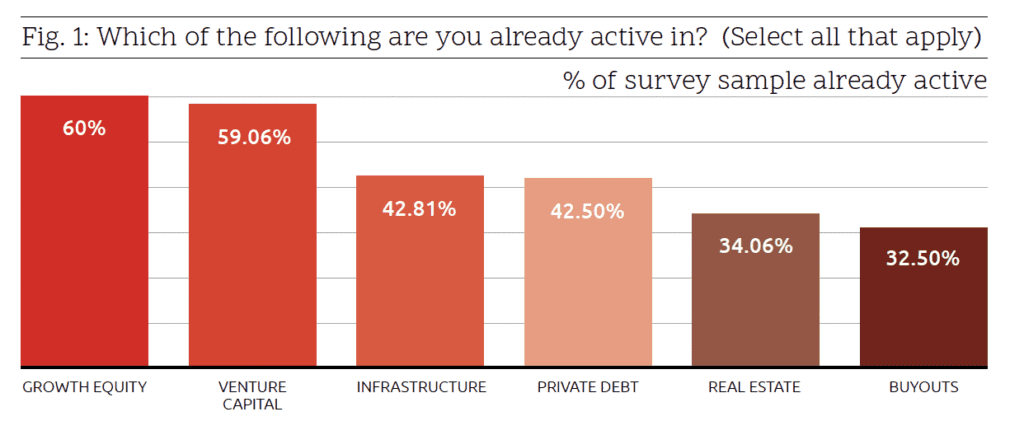

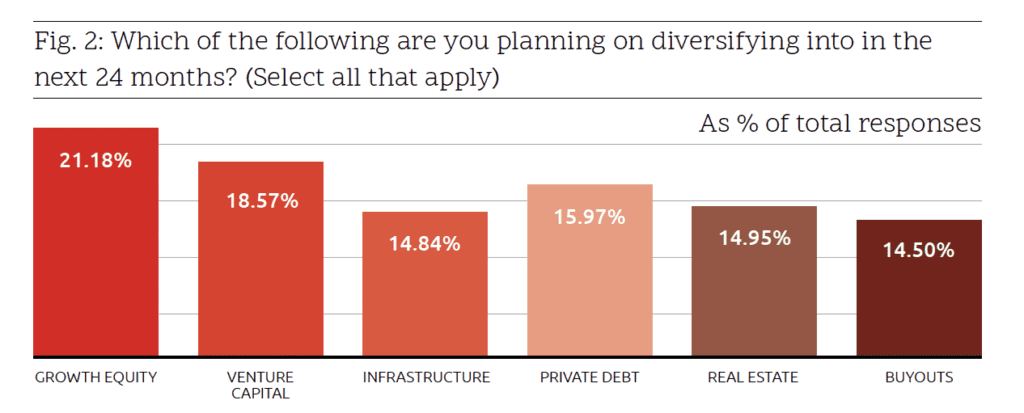

The results of the survey as a whole confirmed several of last year’s findings. Private equity remains the area on the private capital investment spectrum in which firms represented by CFO respondents are most active, followed closely by venture capital (see fig. 1). While this is likely to remain so, expansion is anticipated over the next 24 months in all strategies (see fig. 2).

Though optional, a majority of participating CFO respondents (84%) chose to complete the section of the questionnaire on ESG. This in itself indicates that, regardless of the approach taken to the matter, ESG is definitely on the CFO agenda. In general terms, ESG considerations are recognised as requiring engagement, even if their relative importance may vary from fund to fund and the practical nature of that engagement is yet to be established.

LP attitudes to ESG

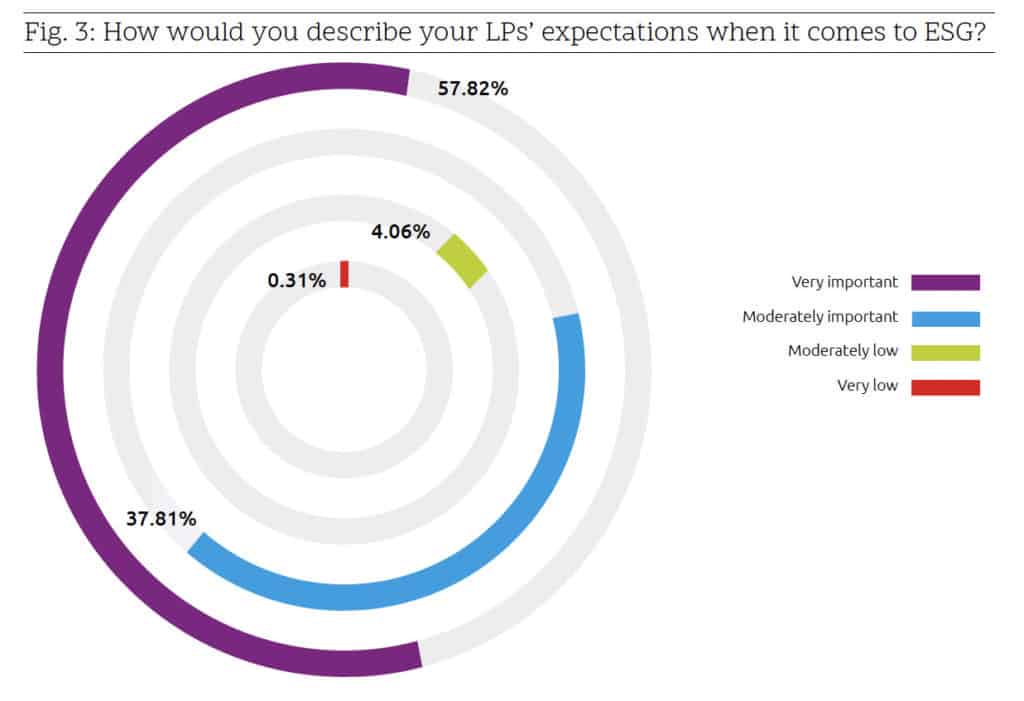

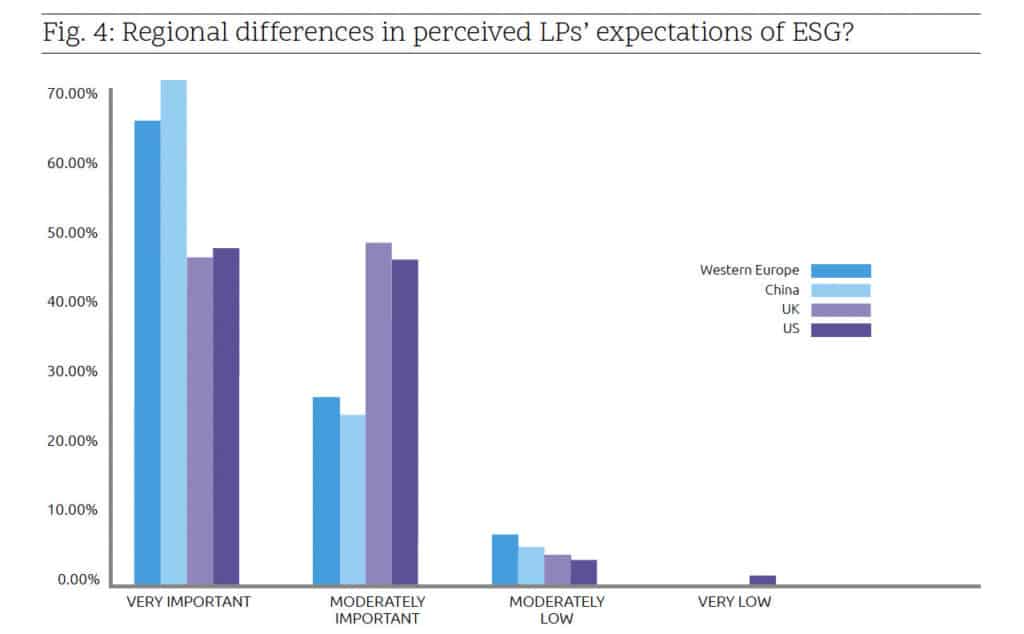

Of the total CFO survey sample, including those who chose not to complete the optional ESG segment of the survey, 58% recognised that ESG was very important to their investors (see fig. 3). Some regional variation was evident (see fig. 4), with US and UK based LPs placing the highest priority on ESG factors, but in all cases, only a tiny minority appeared to give a low priority to ESG concerns.

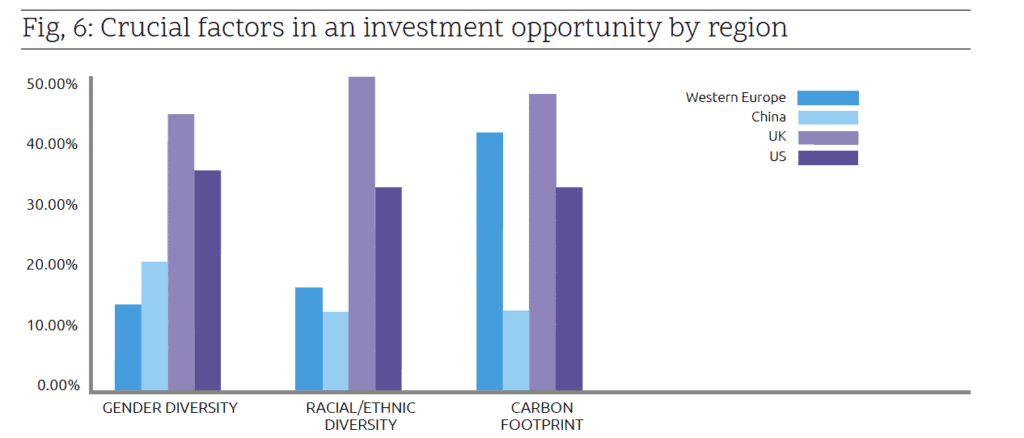

As fig. 5 shows, between 67% and 79% of participating CFOs see gender diversity, racial/ethnic diversity, and carbon footprint considerations as either crucial or important in their assessment of potential investments. Here again, there are regional differences with gender diversity and carbon footprint of most concern to UK CFOs (see fig. 6). In all regions, however, these factors are considered at least ‘somewhat important’. In almost all cases, the percentage of CFOs suggesting any one of them is no more than a consideration is in single figures.

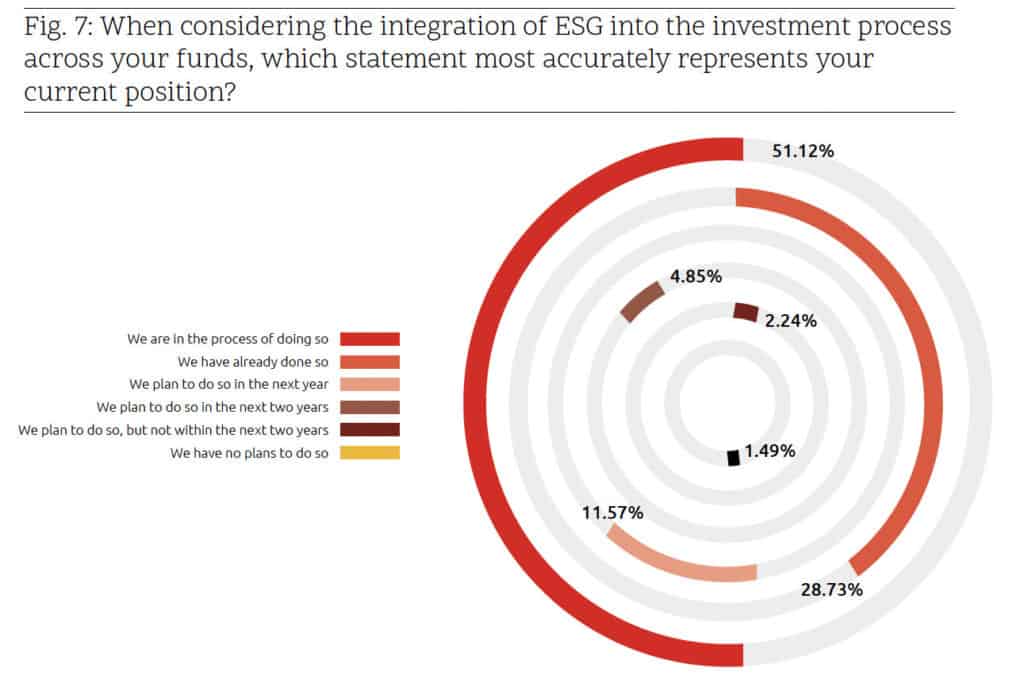

While the principle of including ESG factors in investment decision-making now appears widely accepted, practical implementation is another matter. Survey responses suggest that firm policies on ESG are still in development. Asked if they had a corporate social responsibility (CSR), sustainability or ESG policy in place, almost 85% of respondents said they did. However, more respondents said they were in the process of implementing ESG policies into their investment process than had already done so (see fig. 7).

What’s missing?

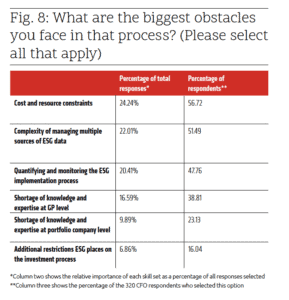

Private capital CFOs clearly recognise the need for a solid framework to manage their ESG data and for the moment, it seems, not many are convinced that they’ve found one. When identifying impediments to ESG integration into their processes, cost and resource constraints were cited as the main obstacles followed by the complexity and variety of ESG data and data sources (see fig. 8).

These factors clearly interrelate. If the data sources are less complex, fewer resources will need to be applied to their management. At the same time, however, the variety of ESG reporting frameworks, which the data will be expected to inform, remains a challenge, with no apparent consensus yet across the industry as to which are the most applicable.

While standards and best practices are, for example, fast developing in areas such as cybersecurity, there is work to be done in developing the same degree of industry consensus on how to define, quantify and report on ESG progress. Regulation may in due course narrow the current levels of fragmentation in this area, but the industry as a whole may benefit from taking the initiative.

What’s changed and what’s the same?

As last year’s exercise found, most private capital CFOs plan to revisit the balance between in-house processes and outsourcing of certain operational functions to support what they consider their firm’s core expertise.

In 2022, expectations from CFOs about required frequency of data updates appears to have decreased slightly in a number of areas. In 2021, for example, 31% of respondents expected their investors to be looking for live updates – or at least access on demand to such updates – on portfolio performance and 27% for live updates on cybersecurity. While results for the latter remain similar, the majority of clients are expected to be satisfied in other areas with daily or weekly information updates. Portfolio performance, operational SLAs and cybersecurity nevertheless remain the top three issues of interest.

It seems that private capital investors may have initially brought with them expectations from the more liquid markets in which they cut their teeth, but that these have lessened over time as comfort and familiarity with the peculiarities of private capital markets become more familiar, coupled with a decrease in levels of investor uncertainty that characterised the earlier stages of the Covid-19 pandemic.

The survey of investors themselves suggests that more than 40% will be wanting live information updates on portfolio performance, while some 55% will be looking for live or daily updates on ESG – 10 percentage points higher than anticipated by CFOs. From an investor perspective, however, the frequency of updates expected could be seen more as a marker of a desire to have access to the data as and when required for monitoring and reporting purposes rather than as specific triggers for action in an investment environment where liquidity is committed for extended periods.